A bill of exchange can function as “legal tender” or “tender of payment,” but its status depends on acceptance and context but regardless, if tendered correctly, it does discharge the debt and respective amount tendered. It is a written instrument where one party (the drawer) orders another (the drawee) to pay a specific amount to a third party (the payee). While bills of exchange can be negotiable, they can also be non-negotiable, meaning they don’t always transfer ownership upon indorsement.

ORIGINAL article on REALWORLDFARE.COM.

1. Definition and Use

A bill of exchange is used primarily in commercial transactions and can either be negotiable (transferable) or non-negotiable (restricted to specific parties). It serves as a promise to pay and can substitute for currency when accepted. The drawer issues it to facilitate payment without using physical cash.

2. Legal Tender and UCC Rules

Under the Uniform Commercial Code (UCC), a bill of exchange does not automatically qualify as legal tender like cash or coins. However, it can still be legally used to settle debts, regardless of whether or not the party receiving the bill of exchange wants to accept it. U.C.C. Article 3 governs bills of exchange, treating them as instruments that may fulfill payment obligations when conditions are met:

- The bill must be signed and clearly list the payment terms.

- It must specify the amount, payee, and payment date.

- The parties involved must agree to its use as a method of settlement.

In this case, the bill becomes legally enforceable and recognized as valid payment, even if it isn’t “legal tender” in the conventional sense.

3. Impact of House Joint Resolution 192 of June 5, 1933, Public Law 73-10, and The Legality of Payment Methods and the Implications

House Joint Resolution 192 of 1933 public law 73-10 establishes that it is “illegal” to demand payment in a specific currency, including cash or coin. This legislation essentially removes the obligation to pay debts in gold or silver, allowing alternative methods of payment, such as bills of exchange.

Demanding specific currency is a direct violation of HJR 192 of 1933 public law 73-10, against the law and a violation of rights “under color of law.” This phrase refers to actions taken by a financial institution and/or person that misuses their authority, leading to a deprivation of rights. By pretending that one can enforce payment in a specific currency, an entity is exerting unlawful pressure on individuals, thus extorting, coercing, and injuring them, and the entity is is infringing upon their rights and legal protections. This action is not only unjust but also contrary to established law and legal standards that recognize alternative forms of payment as valid.

The demand for specific currency payment is not only inconsistent with HJR 192 and the U.C.C. but also constitutes a form of legal overreach that deprives individuals of their rights.

4. UCC 3-104: Defining Negotiable Instruments

UCC 3-104 defines a negotiable instrument, which is a document that promises payment of money under specific conditions. According to UCC 3-104, for an instrument to be negotiable, it must meet these criteria:

- It must be in writing.

- It must be signed by the maker or drawer.

- It must contain an unconditional promise or order to pay a fixed amount of money.

- It must be payable on demand or at a specific time.

- It must be payable to order or to bearer.

When you accept a BILL (a negotiable instrument) or participate in a trade or use a banker’s acceptance, and/oror indorse and transfer the monetary instrument, you effectively negotiate that instrument, which then serves as “tender of payment.” This means that it can be used to discharge debts just like cash. You assign credit to the company to credit the account.

5. Acceptance and Settlement

To function effectively as legal tender, the payee must accept the bill upon presentment. If it is non-negotiable, the drawee must honor it according to the terms specified without transferring it further. Its effectiveness relies on mutual acceptance, not the instrument’s inherent value.

6. UCC 3-603 and 3-311 Provisions

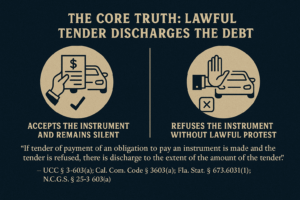

MOST Importantly, U.C.C. § 3-603 stipulates that refusal to accept a valid bill of exchange results in the discharge of the debt amount. This means that if a debtor presents a bill of exchange for payment and the creditor refuses to accept it, the debt is considered discharged. Furthermore, U.C.C. § 3-311 stipulates that if the tender of payment is accompanied by a statement indicating it is for “full satisfaction” of the debt, there is a discharge of the obligation. This further emphasizes the legal significance of a bill of exchange as a valid instrument for settling debts.

Summary

In summary, while a bill of exchange isn’t traditional legal tender, it can and does legally discharge debts, even when refused, and whenever “full satisfaction” is clearly expressed.

SCHEDULE A CONSULTATION.