“Lawful money” is a term used in the Federal Reserve Act, the act that authorizes the Board of Governors of the Federal Reserve System to issue Federal Reserve notes. The Act states that Federal Reserve notes “shall be obligations of the United States and shall be receivable by all national and member banks and Federal reserve banks and for all taxes, customs, and other public dues. They shall be redeemed in lawful money on demand at the Treasury Department of the United States, in the city of Washington, District of Columbia, or at any Federal Reserve bank.” This is also reflected in 12 U.S. Code § 411 – Issuance to reserve banks; nature of obligation; redemption, which stipulates:

“ Federal reserve notes, to be issued at the discretion of the Board of Governors of the Federal Reserve System for the purpose of making advances to Federal reserve banks through the Federal reserve agents as hereinafter set forth and for no other purpose, are authorized. The said notes shall be obligations of the United States and shall be receivable by all national and member banks and Federal reserve banks and for all taxes, customs, and other public dues. They shall be redeemed in lawful money on demand at the Treasury Department of the United States, in the city of Washington, District of Columbia, or at any Federal Reserve bank. “

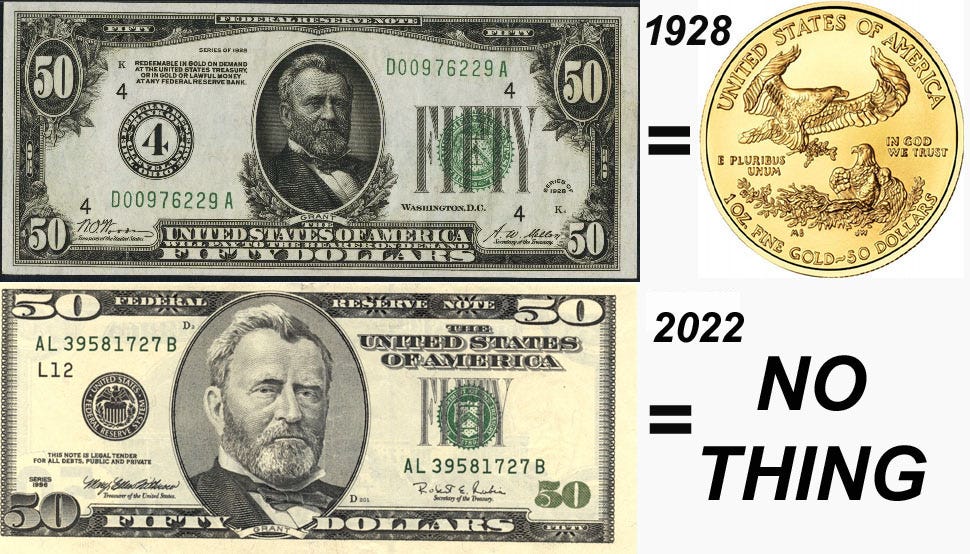

The Act did not, however, define the term “lawful money,” but up until 1913, the only currency issued by the United States that was legally recognized as “lawful money” was various issues of “demand notes” (subsequently known as “old demand notes”) and “United States notes” authorized by Congress during the Civil War.

At the time, some currency was not considered “legal tender,” although it could be used by national banking associations as “lawful money reserves.” Thus, the term “lawful money” had a broader meaning than the term “legal tender.”

In 1933, by way of House Joint Resolution 192 of June 5, 1933, Congress changed the law so that all U.S. coins and currency (including Federal Reserve notes), regardless of when issued, constitutes “legal tender” for all purposes.